The past 2017 is considered to be a policy year for the medical industry and a year of many policies.

In line with the general trend of “distributing the clothesâ€, the conservative medical industry has also produced the fruits of sporadic markets. Among them, "shared medical" and "Medical Mall" have become the "Apple in the eye" of many investors.

But is this really a new format? Such as oral, medical beauty, physical examination, TCM health, eye optometry and other formats that have both medical and consumer attributes, and the retail industry has long been "happy" for many years.

What is "Medical Mall"? What is its connotation and extension? So far, the industry lacks a unified consensus. The author has previously conducted some research on the characteristics and forms of Medical Mall through literature research.

Comrade Xiaoping said well, "No matter black cats and white cats, it is a good cat to catch mice." Whether it is a health city or a shopping mall, it is a brave market-oriented exploration that can integrate medical and retail formats. Therefore, in line with the principle of setting no-limit restrictions, Yingci Medical IHG summarizes four common “retail + medical†models, mainly based on free Americans.

There are several main forms of medical and retail integration in the United States: clinic clusters, retail clinics, medical malls, and individual clinics in general office buildings and shopping malls.

Clinic cluster

The clinic cluster is usually a clinic run by an individual practicing doctor or group of doctors, independent of the hospital, to form a gathering and synergy. This format is prevalent in countries where physicians are free to practice, such as the United Kingdom and the United States.

Typical cases are trusts that offer a combination of basic and specialist medical care, such as the Redbridge Primary Care Trust in England and the Harrow Primary Care Trust. There is also the Polyclinic Group of Doctors in Seattle, Washington, USA.

In the case of The Polyclinic, the group was founded in 1917 and was founded by six doctors. Together, they opened a comprehensive clinic, initially renting a space inside a bank building, setting up X-rays, inspection rooms and outpatient operating rooms.

The Polyclinic's doctors have their own clinics, but share the same block number, providing medical services including cardiology, dermatology, general medicine, gastroenterology, general surgery, internal medicine, nephrology, otolaryngology, medical beauty, lung Services such as department, urology, vaccination, patient education and medical care.

Currently, The Polyclinic has replicated 18 similar clusters in the Greater Seattle area, with approximately 200 general and specialist specialists, and has become the largest multi-specialist group in Puget Sound.

Retail clinic

The retail clinics in the United States appeared around 2000. Due to the low fees, the operation time is longer than that of the hospitals. The staff are mostly nurse practitioners, pharmacists and assistant physicians in price, time, space and personnel. The flexibility is better than the hospital. The “value medical care†that emerged in 2013 has driven the rapid development of retail clinics. According to Accenture, the number of retail clinics in the United States may exceed 2,800 in 2017.

The services of retail clinics are mainly common diseases, frequently-occurring diseases and health management, including colds, coughs, minor injuries, chronic disease management, vaccines, smoking cessation, weight loss, pre-school physical examination, etc. The per capita medical expenses are around US$150.

The data shows that this new format has a significant effect on the diversion and control of US hospitals. According to the National Bureau of Economics, hospital emergency rooms (ERs) near retail clinics have reduced 12.3% of influenza patients and 4.1% of people with diabetes, saving $817,000 per 100,000 population a year.

Retail clinics are mainly operated by retail pharmacies (such as CVS's one-minute clinic) and large department stores (such as Walmart's Walmart Pharmacy), with distinct business characteristics:

The first is standardization, which guides the medical staff's diagnosis and treatment behavior and controls risks by establishing standardized treatment procedures;

The second is synergy, establishing vertical cooperation with the hospital, and providing users with a referral channel to the hospital when encountering problems beyond the service capacity. For example, CVS's one-minute clinic has established a partnership with the Cleveland Clinic;

The third is flexibility. With more placements and longer operating hours, retail clinics have unlocked the service needs of residents. For example, in 2016, in Shanghai Pudong, the United States retail clinic brand FastMed landing day surgery comprehensive outpatient clinic Yushimeidi, treatment time extended from 9:00 am to 11:00 pm Monday to Friday, 9:00 am to 18:00 on weekends 5 o'clock. According to a report released by Rand in 2016, between 2011 and 2012, Antai has nearly one-third of health insurance users in the year, at least because of “low-acuity conditionsâ€. The clinic saw a disease and the number of total visits by users increased significantly.

Individual clinics in ordinary office buildings and shopping malls

Some of the less risky and profitable departments have long been independent of hospitals, scattered among the major office buildings and shopping malls. Unlike clinic clusters, retail clinics and Medical Mall, these individual clinics are usually independent and lack uniformity. The launch and operation of the mall, the mall lacks a top-level design for medical care.

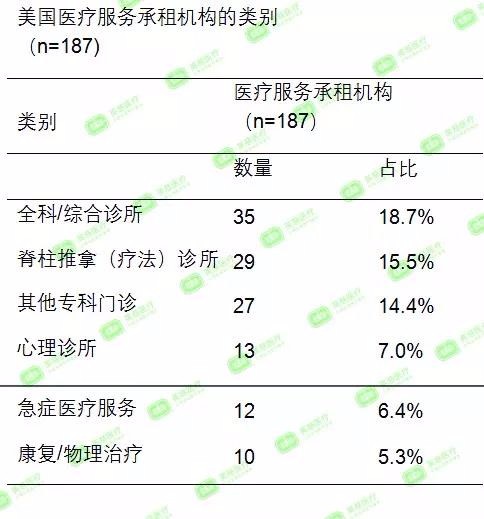

A paper "On call at themall: a mixed methods study of US medical malls" surveyed 1395 malls with medical formats, of which 870 (62.4%) had optometry stores and 241 (17.3%) had dental clinics. . In addition to the most common optometry and dentists, there are 89 other malls offering other medical services. The largest of these are general and massage clinics, accounting for 18.7% and 15.5% respectively. Psychological clinics, emergency, rehabilitation, and fitness accounted for less than 7%.

Source: On call at the mall: a mixed methods study of US medical malls

Medical Mall

Most of the US Medical Mall sponsors are hospitals. This is related to the unique medical market environment in the United States.

For American hospitals, the main driving forces for opening the Medical Mall are:

1) Under the premise of not building a new hospital and renovating the old courtyard, it will provide space for the development of new services and the configuration of new equipment;

2) Provide day treatment services and inspection and diagnosis services at the same location;

3) Expand the service radius and fill the gaps in areas with insufficient medical services;

4) Provide office space for doctors;

5) Increase the access channel.

In recent years, retail clinics have grown stronger. Under the pressure of competition, hospitals have begun to provide patients with more convenient medical choices and increased access to tourists. Medical Mall is equivalent to the “satellite clinic†of large hospitals, similar to retail hypermarkets. “Satellite convenience store†(traditional hypermarkets such as Carrefour, Tesco, and Yonghui Supermarket have created their own convenience store brands, expanding their reach into the 15-minute radius service circle).

The Jackson Medical Mall in Jackson City, Miss., is the first medical mall in the United States. Its predecessor was an abandoned mall. In 1996, the University of Mississippi Medical Center (UMMC) led a transformation of the mall and built a multi-disciplinary, non-profit medical mall.

The modified Medical Mall covers an area of ​​850,000 square feet, including eight medical specialties - pediatrics, general, gastroenterology, internal medicine, rheumatology, endocrinology, maternal and child care, and pulmonary medicine; four nursing and pharmacy colleges. The mall and 10 hospitals have cooperation, and 11 individual doctors have settled in, and 8 commercial insurances have been docked. The average waiting time for patients to visit a doctor in the mall is 16 minutes (the national average waiting time is 21 minutes).

The Medical Mall is also housed in grocery stores, community development centers, restaurants, beauty salons, shoe stores, social service agencies, banks and educational institutions.

Local residents are mainly low-income African Americans, and travel depends on public transportation. Previously, local medical and employment needs were not met. Jackson Medical Mall has become a gathering place with medical services as the main body, while providing multi-social public services and meeting certain consumer needs.

Of course, the originator of the US Medical Mall is not limited to hospitals, but also doctor groups and investors. The operational management model after the reconstruction is also different. Yingci Medical has summarized this. For details, see the private pioneer Medical Mall.

Why is the stone of other mountains attacking jade?

It should be noted that in addition to the individual clinics in ordinary office buildings and shopping malls, the above three “retail + medical†formats depend on the special medical environment in the United States. This particularity is mainly reflected in:

The hospital mainly provides inpatient services, and the outpatient clinic is provided by an individual doctor or doctor group that rents the venue at the hospital.

Clinics and urgent care usually do not have a pharmacy. After the doctor prescribes the patient, the patient needs to go to the retail pharmacy outside the hospital to purchase the medicine.

The medical payment party in the United States is mainly employer commercial insurance, covering about 2/3 of the population. The medical insurance provided by the government is only for the elderly and the poor who are over 65 years old, the disabled, the veterans, etc., covering about 1/3 of the population.

Doctors are free to practice, most of them run their own clinics, or a group of small doctors who make up 2-10 people, and a few are employed in hospitals.

The US insurance industry is strong and has strong bargaining power. The Obama medical reform environment has raised the value-oriented medical payment method, which has increased the pressure on medical service providers. The doctor group has a tendency of horizontal and vertical integration, and doctors also have a tendency to return to large hospitals.

This special medical environment has created an opportunity for the development of new medical formats in the United States, both of which address the two major challenges of accessibility and cost control.

Not suffering from unequalness. The level of doctors is uneven, and high-quality medical resources are highly concentrated in large cities and large hospitals. This is the main contradiction faced by Chinese patients for medical treatment.

Therefore, clinic clusters, retail clinics, and Medical Mall, whether they have a suitable living soil in China, how to localize is a problem that Chinese practitioners need to think about.

Reference materials:

Partners for Livable Communities, Jackson Medical Mall, extracted from http://livable.org/livability-resources/best-practices/150-jackson-medical-mall%20on%20Dec%2004

Uscher-Pines et al. , Oncall at the mall: a mixed methods study of US medical malls

The Polyclinic, extracted from https://polyclinic.com/insurance-billing

American Medical Association, 2016 Physician Benchmark Survey

Villager's Diary Latitude Health, "Service Capability Positioning of New Clinics: Can Do and Can't Do"

10' Pvc Coated Gloves,Pvc Double Dipped Gloves,Tough Flexible Pvc Gloves,Open Back 3/4 Coated Gloves

JINAN SHANDE SECURITY TECHNOLOGY CO., LTD , https://www.sdsxlb.com